Goods Transportation in India

The most popular form of goods transport in India is via road. As per the National Highways Authority of India, about 65% of freight and 80% passenger traffic is carried by the roads. Transportation of goods by road is done by transporter or courier agency. This article will discuss the transporter, i.e, the GTA.

What service of transportation of goods is exempt under GST?

Services by way of transportation of goods are exempted:

- by road except the services of:

- a goods transportation agency;

- a courier agency

- by inland waterways.

Therefore, the service of transportation of goods by road continues to be exempt even under the GST regime. GST is applicable only on goods transport agencies, GTA.

What is a GTA?

As per Notification No. 11/2017-Central Tax (Rate) dated 28th June, 2017, “goods transport agency” or GTA means any person who provides service in relation to transport of goods by road and issues consignment note, by whatever name called. This means, while others might also hire out vehicles for goods transportation, only those issuing a consignment note are considered as a GTA. Thus, a consignment note is an essential condition to be considered as a GTA.

What is a consignment note?

A consignment note is a document issued by a goods transportation agency against the receipt of goods for the purpose of transporting the goods by road in a goods carriage. If a consignment note is not issued by the transporter, the service provider will not come within the ambit of the goods transport agency.

If a consignment note is issued, it means that the lien on the goods has been transferred to the transporter. Now the transporter is responsible for the goods till it’s safe delivery to the consignee.

A consignment note is serially numbered and contains –

- Name of consignor

- Name of consignee

- Registration number of the goods carriage in which the goods are transported

- Details of the goods

- Place of origin

- Place of destination.

- Person liable to pay GST – consignor, consignee, or the GTA.

What are the services provided by a GTA?

The service includes not only the actual transportation of goods, but other intermediate/ancillary service provided such as-

- Loading/unloading

- Packing/ unpacking

- Trans-shipment

- Temporary warehousing etc.

If these services are included and not provided as independent activities, then they are also covered under GTA.

What was the situation under Service Tax?

RCM applied under the Service tax laws too. There was an abatement of 60% (40% taxable) for transportation of used household goods and 70% (30% taxable) for transportation of normal goods.

What is the rate of GST on GTA?

Service by a GTAGST rateCarrying-agricultural producemilk, salt and food grain including flour, pulses and riceorganic manurenewspaper or magazines registered with the Registrar of Newspapersrelief materials meant for victims of natural or man-made disastersdefence or military equipment0%Carrying- goods, where consideration charged for the transportation of goods on a consignment transported in a single carriage is less than Rs. 1,5000%Carrying- goods, where consideration charged for transportation of all such goods for a single consignee does not exceed Rs. 7500%Any other goods5% No ITC OR 12% with ITCUsed household goods for personal use0% **Transporting goods of unregistered personsEarlier exempted, but later made taxable; currently, list yet to be notified**Transporting goods of unregistered casual taxable personsEarlier exempted, but later made taxable; currently, list yet to be notified**Transporting goods (GST paid by GTA)*5% No ITC or 12% with ITCTransporting goods of 7 specified recipients*if GTA Charges 12%, GTA must deposit tax and ITC can be availed.Otherwise if GTA Charges 5%, RCM applies and recipient must deposit tax and ITC cannot be availedHiring out vehicle to a GTA0%

*As per Notification No. 20/2017-Central Tax (Rate) 22nd August, 2017

** On 31st Dec 2018, The Government cancelled Notification No. 32/2017- Central Tax (Rate) dated 13th October, 2017, thereby making purchase from unregistered dealers taxable. However, the list of registered persons or transactions is yet to be notified.

Is a GTA liable to register?

There was a lot of confusion about whether a GTA has to register under GST. As per Notification No. 5/2017- Central Tax dated 19/06/2017, a person who is engaged in making only supplies of taxable goods/services on which Reverse Charge Mechanism (RCM) applies is exempted from obtaining registration under GST.

Thus, a GTA does not have to register under GST if he is exclusively transporting goods where the total tax is required to be paid by the recipient under reverse charge basis (even if the turnover exceeds the threshold limit).

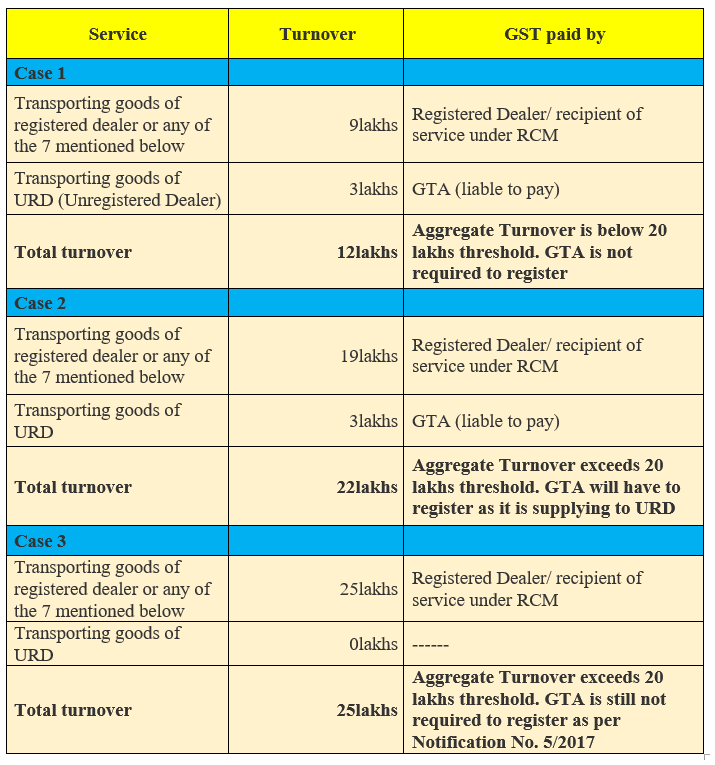

Scenarios for Registration for a Goods Transport Agency*

* The threshold for GST registration has been increased to Rs.40 lakh for supply of goods.

Who pays GST while hiring a GTA?

If a GTA provides the services to the certain businesses, recipient of services is required to pay GST under reverse charge.

Which businesses are liable to pay GST under reverse charge for a GTA?

The following businesses (recipient of services) is required to pay GST under reverse charge:-

- Factory registered under the Factories Act,1948;

- A society registered under the Societies Registration Act, 1860 or under any other law

- A co-operative society established under any law;

- A GST registered person

- A body corporate established by or under any law; or

- A partnership firm whether registered or not (including AOP)

- Casual taxable person

Who will pay under Reverse Charge?

As per Notification No. 13/2017- Central Tax dated 28/06/2017 the person who pays or is liable to pay freight for the transportation of goods by road in goods carriage, located in the taxable territory shall be treated as the receiver of service.

Payment is by sender

If the supplier of goods (consignor) pays the GTA, then the sender will be treated as the recipient. If he belongs to the category of persons above then he will pay GST on reverse charge basis.

Payment by Receiver

If the liability of freight payment lies with the receiver (Consignee), then the receiver of goods will be treated as a receiver of transportation services. If he belongs to any of the above category of persons, then he will pay GST on reverse charge basis.

Various Scenarios to Determine Who is Liable to pay GST in case of a GTA

Service ProviderSupplier/ ConsignorReceiver of goods/ ConsigneePerson paying FreightPerson liable to pay GSTGTAA company (Whether or not registered under GST)Partnership Firm (Whether or not registered under GST)CompanyCompanyGTAPartnership Firm (Whether or not registered under GST)Registered Dealer XXXGTAPartnership Firm (Whether or not registered under GST)Registered Dealer XFirmFirmGTAA Co-Op Society Ltd (Whether or not registered under GST)Registered Dealer XXXGTAA Co-Op Society Ltd (Whether or not registered under GST)Registered Dealer XA Co-Op Society LtdA Co-Op Society LtdGTACompany A Ltd. (Whether or not registered under GST)Company B Ltd. (Whether or not registered under GST)B LtdB LtdGTAURD ARegistered Dealer XAXGTAURD ARegistered Dealer XXXGTAURD AURD FFExempted**

** GTA services to an unregistered person is exempted as per Notification No. 32/2017- Central Tax (Rate) dated 13th October 2017. However, this notification is cancelled as of 31st Dec 2018 and hence, tax must be paid under RCM for unregistered purchases on the notified list of supplies. However, the list is yet to be notified.

Reverse Charge if the GTA Is Unregistered

As per Notification No.32/2017-Central Tax (Rate) dated 28th June 2017, intra-state supplies of services or both received by a registered person from any unregistered supplier, was exempted from GST if it does not exceed Rs. 5,000 in a day. However, the Government has cancelled the notification and hence, RCM applies on unregistered purchases for only a specified list of supplies, which is yet to be notified.

Input Tax Credit

If GTA pays GST

GTA has 2 options-

- 12% GST with ITC *

OR - 5% GST with no ITC*

However, the GTA has to opt in at the beginning of the financial year.

*As per Notification No. 20/2017-Central Tax (Rate) 22nd August, 2017

If Service Receiver pays GST under RCM

Service receivers can always avail ITC on GST paid under RCM.

Invoicing for GTA

Any GST compliant invoice of a GTA must have following details-

- Name of the consignor and the consignee

- Registration number of goods carriage in which the goods are transported

- Details of goods transported

- Gross weight of the consignment

- Details of place of origin and destination

- GSTIN of the person liable for paying tax whether as consigner, consignee or goods transport agency

- Name, address and GSTIN (if applicable) of the GTA

- Tax invoice number (it must be generated consecutively and each tax invoice will have a unique number for that financial year)

- Date of issue

- Description of service

- Taxable value of supply

- Applicable rate of GST (Rates of CGST, SGST, IGST, UTGST and cess clearly mentioned)

- Amount of tax (With breakup of amounts of CGST, SGST, IGST, UTGST and cess)

- Whether GST is payable on reverse charge basis

- Signature of the supplier

Payment of Tax by a GTA

A GTA cannot enjoy any ITC on any of the inputs. So, payment of tax will be only through cash in the normal modes of card/netbanking/cash (only for taxes upto Rs.10,000).

Returns to be Filed by a GTA

If all the services of the GTA fall under RCM then a GTA is not required to register. If a GTA registers, then it will have to file the normal 3 monthly returns – GSTR-1 (sales), GSTR-2 (purchases-no ITC available) & GSTR-3 (monthly summary & tax liability).

How to determine Place of Supply for a GTA

The place of supply of services by way of transportation of goods, including by mail or courier to–– (a) a registered person, shall be the location of such person (b) a person other than a registered person, shall be the location at which such goods are handed over for their transportation.

Examples for determining place of supply

Rajesh is a registered dealer in Bangalore. He hires a GTA to deliver goods to Mumbai.

Place of supply will be Bangalore.

Anita is an unregistered dealer in Gujarat who hires a GTA to deliver goods to Rajasthan.

Place of supply will be Gujarat where Anita hands over the goods to the transporter.

Vikas is registered in both Mumbai and Bangalore. He hires a transporter (based in Mumbai) to deliver from Bangalore to Delhi.

CGST & SGST will be applicable. If the transporter is based in Chennai, then IGST will be applicable.

Frequently Asked Questions

Ajay hired a GTA to transport his goods. The consideration charged was Rs. 1,200. Will Ajay pay GST?

Ajay will not pay GST under RCM as the consideration for transportation of goods on a consignment transported in a single carriage is less than Rs. 1,500.

Vinod hired a GTA to transport goods. The GTA was asked to come 2 days as Vinod would receive the goods in batches. The entire consideration was Rs. 600. Will Vinod pay GST?

Vinod will not pay GST because the consideration charged for transportation of all such goods for a single consignee does not exceed Rs. 750.

Mr. Ajay, a working professional, is moving houses and hires XYZ GTA to transport his household items. XYZ demands Ajay to pay GST under RCM as moving charges are Rs. 6,000. Ajay is confused.

Ajay is unregistered and if XYZ GTA is also unregistered under GST then, GST is not applicable. If XYZ is registered, then it will pay GST of 5%. RCM will not apply on Ajay.

Anand, a garments shop owner in Kolkata, hires a truck to deliver goods from wholesaler to his (Anand’s) shop. Anand’s turnover is less than 20 lakhs and he has not registered under GST. The GTA demands that Anand should pay tax under RCM. Anand argues that since he is not registered, he does not have to pay any GST.

Only the persons above (Notification No. 13/2017- Central Tax (Rate) dated 28th June, 2017) are required to pay GST under RCM. Unregistered dealers (Anand) purchasing goods/services from unregistered GTA do not have to pay GST under reverse charge mechanism. If the URD hires from a registered GTA, then the registered GTA is liable to pay GST. So, Anand is not liable to pay GST under RCM.

Anand now purchases garments from Assam and pays for a truck to deliver the goods to his shop in Kolkata. The GTA says that Anand has to register for GST as he is making an inter-state purchase as only registered dealers can have inter-state trade.

An unregistered person can make inter-state purchases. For making inter-state sales, he will have to be compulsorily registered. Since Anand is an unregistered dealer and the GTA is also unregistered then the concept of RCM does not arise.

The GTA is registered at Assam and its branch is collecting cash in Kolkata on his behalf. Recipient of service Anand is in Kolkata. If Anand was registered, would he have charged IGST or SGST/CGST under RCM?

If the original transporter in Assam bills Anand, then IGST should be charged. If he bills the branch then SGST/CGST will apply.

Anand has received a one-time contract to sell garments to a dealer in Mumbai. Anand hires a truck to send the goods.

Since, Anand is not registered under GST, he cannot make any inter-state sale. To make an inter-state sale, he must register as a casual taxable person. Then when he hires a truck to send the garments, automatically he is liable to pay GST under RCM.

Anand is sick of all this and decides to voluntarily register. He hires a truck again to transfer goods from the wholesaler to his shop. GTA asks him to pay GST on RCM as he is registered. But Anand’s view is that his turnover is still below 20 lakhs.

The threshold of turnover does not matter if a person is voluntarily registered. All provisions of the GST Act will apply to a registered person. Anand is liable to pay GST under RCM.

Anand’s turnover has increased to 45 lakhs. He wants to shift to composition schemes as he sells mainly to end consumers. But he is worried as his GTA has told him they would not deliver his goods if he is registered under composition scheme as the GTA becomes liable for GST.

This is a myth. Even composition dealers are liable to pay GST under RCM. Anand will pay GST on RCM if he hires a GTA whether he is registered as a composition dealer or as a normal dealer.

The concept of RCM on GTA was also there under service tax. Pure transportation of goods services is mostly provided by the unorganised sector and hence they have been specifically excluded from the tax net. In respect of GTA, the liability to pay GST falls on the recipients under reverse charge in most of the cases. However, the GTA may opt to pay under forward charge.

However, transporters were confused in the beginning due to the law “persons who are required to pay tax under reverse charge” have to be compulsorily registered. Transporters refused unregistered dealers because they were afraid they would have to register. The government issued more clarifications & FAQs addressing the GTAs on this, to reduce such confusions.